Summary

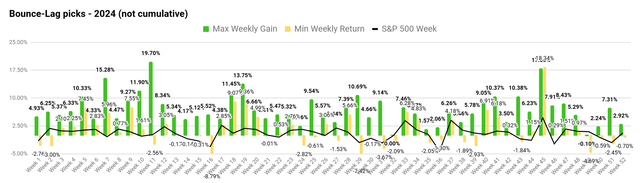

- The Bounce/Lag Momentum model achieved a 211.48% YTD simulated portfolio return in 2024, significantly outperforming major indices and demonstrating its effectiveness in stock-picking.

- Weekly portfolios are created and measured separately, in a multi-year father/son competition to deliver the best performance between Grant’s Bounce-Lag algorithm and JD’s MDA breakout model.

- Momentum Gauges continue in high negative signals starting on December 12th and the weekly gauges continue negative for the first time since September.

- As a reminder, the B/L picks gained +47.6% in 2022 using the Momentum Gauges in the worst markets since 2008 with S&P 500 down -19.44%, Nasdaq -33.10% and Russell -21.56%.

- Stocks can be radically different from each other. Members are encouraged to follow the first 2 steps in the Getting Started Instructions to build an optimal portfolio mix for your own best risk/return tolerance.

This is a special contribution article by Prof. Grant Henning based on his published research on the B/LM technical theory. The model and comments are expressly based on his own proprietary methodology and forecasts in the references below. These selections are exclusively for members.

Grant has agreed to extend his bonus weekly Bounce/Lag picks into 2025 as an additional feature to my Value & Momentum Breakout service. Our father-son weekly competition will continue into a 5th consecutive year!

The Bounce/Lag average cumulative returns increased to 211.48% YTD to end the 5th year of annual measurements of Grant’s model on SA. This is a weekly average between the best case weekly cumulative returns of +354.6% and worst case equal-weighted fixed buy/hold return of +68.3% through negative signals. Each week is a separate portfolio and results are added together. Each weekly return is a separate portfolio and could also be compounded weekly for measurement purposes.

The Weekly Bounce/Lag Momentum picks for 2024